Florida property insurance experts cautiously

optimistic ahead of hurricane season

And as with every hurricane

season, it only takes one storm to upend years of work that

industry officials say helped attract 20 new property and

casualty insurance companies with more than $850 million in new

capital into the state’s market. |

|

Article Courtesy of News Service of Florida

By Jim Turner

Published June 3, 2026

|

WATCH VIDEO |

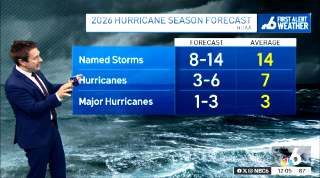

A "below-normal" year for storms could further a

positive trend for Florida's insurance market, industry experts contend.

But because of Florida’s location between the Atlantic and Gulf,

homeowners will always be at risk, which will temper any potential

reductions to premiums.

|

Heading into the Atlantic storm season

that begins June 1, insurance experts said legislative

reforms in 2022 and 2023 targeting “frivolous” lawsuits,

along with a year without any storm hits, have allowed some

“softening” in homeowners insurance prices, growth in new

carriers into the state, and a fall in the policy count by

state-backed Citizens Property Insurance from 1.41 million

policies in October 2023 to 336,000.

“We are just becoming more and more resilient in the state.

So, I’m kind of optimistic that, as we see the next storm,

we are going to be in better shape than we have been in the

past,” said Patricia Born, who is the Midyette Eminent

Scholar in Risk Management and Insurance at Florida State

University’s Herbert Wertheim College of Business.

The industry is further helped right now from a “soft cycle”

for reinsurance, the insurance for insurers.

But don’t anticipate any decline to erase the sharp rise in

premiums Florida residents endured in the last 10 years,

according to the nonprofit Coalition for an Insurable

Future.

|

|

NBC6’s Adam Berg reports on the forecast, a 55%

chance for a below-average season.

|

And as with every hurricane season, it only takes one

storm to upend years of work that industry officials say helped attract

20 new property and casualty insurance companies with more than $850

million in new capital into the state’s market.

On May 20, Insurance Commissioner Mike Yaworsky and Chief Financial

Officer Blaise Ingoglia announced the three latest property and casualty

insurers entering Florida’s market: Texas-based Builder Reciprocal

Insurance Exchange, Lake Mary-based Frontline Insurance Reciprocal

Exchange and Arizona-based Wingsail Insurance Company.

“Competition is the best way to ensure that Floridians can access the

best coverage at the best price,” Ingoglia said in a released statement.

Born said while the industry looks strong, the Florida market needs more

nationwide providers.

“We would prefer that more insurers that have a footprint across the

whole country would be writing in Florida, so that they’re diversified

more broadly,” Born said.

Chris Dittman, executive managing director for Dothan, Alabama-based Aon

Corporation, said the reforms in Florida have resulted in sustained

profitability.

"Florida is a very risky state, and it is the peak risk in the world,

and so there is underwriting income needed in these (non-catastrophe)

years to pay for the (catastrophe) losses, because those will happen,”

Dittman said during a media call hosted by the AM Best insurance ratings

firm.

Lawmakers in 2022 and 2023 eliminated one-way attorney fees and banned

assignment of benefits, where contractors would take over policyholder

claims. The efforts also imposed larger rate increases for customers of

the Citizens Property Insurance Corp., to bring rates closer to private

carriers and reduce the number of policies held by the state-backed

insurer.

An AM Best report out last week said Florida’s market had stabilized and

called it an “increasingly manageable market.”

The report stated Florida-domiciled personal property specialist

companies recorded nearly $1 billion in underwriting gains, a vast

improvement from the $132 million underwriting loss two years earlier.

“The improved Florida property insurance landscape reflects reduced

litigation and claim solicitation, attracting new writers to the state

while allowing existing writers to recover from losses in earlier years

and take advantage of more refined pricing sophistication,” said Lauren

Magro, AM Best senior financial analyst. “While 2024 marked the first

year of an underwriting profit for the segment in over a decade, results

in 2025 only further extended this trend and benefited from no named

hurricanes making landfall.”

|